You can't protect what you don't know you have, and you can't prioritize compliance efforts without understanding your actual risk exposure. Yet most SMBs skip formal risk assessments—and pay the price when auditors demand evidence.

You can’t protect what you don’t know you have, and you can’t prioritize compliance efforts without understanding your actual risk exposure. Yet most SMBs skip formal risk assessments—and pay the price when auditors demand evidence.

We’ve seen it happen too many times. A business owner gets that dreaded notice. An audit is coming. Suddenly, everyone’s scrambling to piece together documentation that should have existed all along. The auditor asks about risk assessments. Blank stares follow.

Here’s the thing: a compliance risk assessment isn’t some bureaucratic checkbox exercise reserved for Fortune 500 companies. It’s how we figure out where we’re vulnerable, what could go wrong, and what actually deserves our limited time and budget. Without it, we’re just guessing.

Let’s fix that.

Key Takeaways

- Most SMBs skip formal compliance risk assessments and face consequences during audits or incidents.

- A compliance risk assessment identifies which regulations apply to your business and where you’re most vulnerable.

- The process involves listing assets and processes, mapping regulations, evaluating likelihood and impact, and prioritizing risks.

- You don’t need expensive consultants—a simple spreadsheet template works for most small businesses.

- Regular reassessment (quarterly or when business changes) keeps your compliance efforts relevant and effective.

Why We Actually Need Compliance Risk Assessments

Let’s be honest. Nobody wakes up excited to do a compliance risk assessment. It sounds boring. It sounds complicated. And when you’re running a small business, it sounds like something that can wait until next quarter.

Except it can’t.

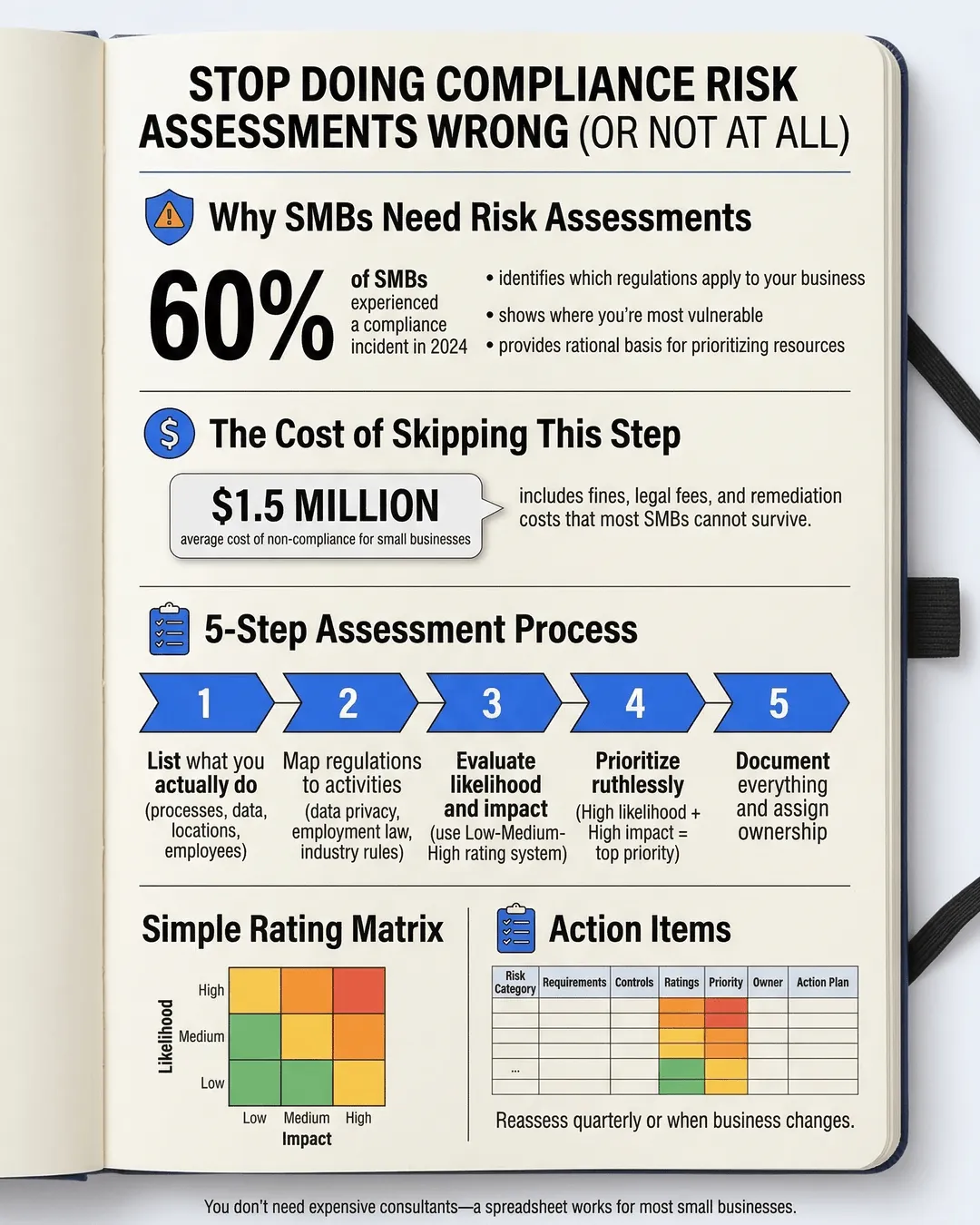

According to Gartner, 60% of small and midsize organizations experienced at least one compliance-related incident in 2024¹. Many of those incidents could have been prevented with basic risk assessment practices.

Here’s what happens when we skip this step. We treat all compliance requirements equally. We spend the same energy worrying about minor record-keeping rules as we do about regulations that could actually shut us down. We miss gaps in our processes because we never mapped them out. And when something goes wrong, we have no documented evidence that we tried to prevent it.

A compliance risk assessment does three critical things. First, it tells us which regulations actually apply to our business. Not every rule affects every company. Second, it shows us where we’re most exposed. Maybe our data security is solid, but our employee classification practices are a disaster waiting to happen. Third, it gives us a rational basis for prioritizing our limited resources.

Insurance companies understand this. Businesses that can demonstrate regular risk assessments often qualify for better rates on errors and omissions coverage. Regulators understand this too. A documented risk assessment process can mean the difference between a warning and a penalty when violations occur.

We’re not talking about achieving perfection. We’re talking about knowing where we stand.

How to Conduct a Compliance Risk Assessment (Without Losing Your Mind)

The good news is that a basic compliance risk assessment doesn’t require a law degree or expensive software. The process follows a straightforward pattern that works for most SMBs.

Start by listing what you actually do. Write down your core business processes, the types of data you handle, where you operate, and what kinds of employees you have. This isn’t a theoretical exercise. We’re mapping reality, not aspirations.

For example, if you run a marketing agency, your list might include: client data storage, employee remote work arrangements, contractor payments, email marketing campaigns, and website analytics. Each of these touches different regulatory areas.

Map regulations to your activities. This is where it gets specific. For each business activity, identify which laws and regulations apply. A compliance risk management framework for SMBs should cover the basics: data privacy (GDPR, CCPA, state laws), employment law (FLSA, ADA, state labor codes), industry-specific regulations, tax requirements, and contractual obligations.

You don’t need to become an expert in each area. But you do need to know they exist and have a general sense of what they require. Many industry associations publish compliance checklists that make this easier.

Evaluate likelihood and impact. For each regulatory requirement, ask two questions. How likely are we to violate this? And if we do, how bad would the consequences be?

A simple three-tier system works well. Likelihood: Low, Medium, High. Impact: Low (minor fines or warnings), Medium (significant penalties or legal costs), High (business-threatening fines or criminal liability).

According to Ponemon Institute research, the average cost of non-compliance for small businesses reached $1.5 million in 2024². That number includes fines, legal fees, and remediation costs. For most SMBs, that’s not survivable.

Prioritize ruthlessly. Anything that scores High on both likelihood and impact goes to the top of your action list. These are your critical risks. Medium likelihood and High impact come next. Low impact items go at the bottom, regardless of likelihood.

This prioritization matters because we can’t fix everything at once. A regulatory risk assessment process helps us focus on what actually threatens the business.

Document everything. Use a risk assessment template for small business tracking. A simple spreadsheet works. Columns should include: Risk Category, Specific Requirement, Current Control Measures, Likelihood Rating, Impact Rating, Priority Level, Owner, and Action Plan.

The template doesn’t need to be fancy. It needs to exist and be updateable.

Assign ownership. Every identified risk needs a person responsible for managing it. This doesn’t mean one person handles all compliance. It means someone owns the monitoring and reporting for each area.

For a small team, this might mean the office manager owns HR compliance, the IT person owns data security, and the owner retains oversight of financial and contractual obligations.

Common Mistakes (That We’ve Definitely Made)

We’ve learned these lessons the hard way, so you don’t have to.

Doing it once and forgetting about it. Your business changes. Regulations change. A risk assessment from two years ago is probably worthless. We recommend quarterly reviews for most SMBs, with immediate updates when you add new services, enter new markets, or change how you handle sensitive data.

Making it too complicated. We’ve seen 50-page risk assessment documents that nobody reads or maintains. Complexity is the enemy of compliance. If your process is so involved that you avoid updating it, you’ve defeated the purpose.

Ignoring “small” risks that add up. A bunch of Low/Low risks can collectively create a Medium/High problem. If you have 15 minor compliance gaps, the cumulative probability that one will cause trouble approaches certainty.

Relying entirely on templates. Generic templates help you start, but your risk profile is unique. A risk assessment template for small business use should be adapted to your specific industry, location, and operations.

Skipping the enforcement research. Some regulations are heavily enforced. Others exist on paper but rarely result in actions against SMBs. Understanding enforcement priorities helps us allocate resources rationally. For instance, the DOL recovered $274 million in back wages for workers in 2024, with small businesses representing 68% of violations³. Wage and hour compliance deserves attention.

Treating compliance as IT’s problem. Technology controls are important, but many compliance risks are process and people issues. Misclassifying employees, missing required posters, improper record retention—these aren’t solved with software.

Making It Actually Work

The difference between a compliance risk assessment that helps and one that gathers dust comes down to integration.

We build risk assessment into existing business reviews. When we do quarterly planning, compliance risks get discussed alongside sales targets and operational challenges. When we’re evaluating a new product launch or market expansion, we run through the compliance implications before making commitments.

A practical example: We were considering adding a subscription billing model to our services. During our risk assessment review, we identified that this would trigger new data retention requirements, recurring payment compliance rules, and auto-renewal disclosure laws in several states. We adjusted our timeline to build those controls before launch, not after.

We also use risk assessment findings to justify budget requests. When you can show leadership that a High/High risk exists and requires investment to mitigate, it’s easier to get approval than vague requests for “compliance improvements.”

Technology helps, but it’s not required. Many excellent compliance management platforms exist, but they’re overkill for companies under 50 employees. A shared spreadsheet that gets reviewed regularly beats expensive software that nobody uses.

Consider appointing a compliance champion, even if it’s not a full-time role. This person keeps the risk assessment updated, tracks regulatory changes in your industry, and reminds everyone when reviews are due.

The regulatory risk assessment process becomes routine when it’s brief, relevant, and connected to decisions you’re already making.

Conclusion

A compliance risk assessment isn’t glamorous work. It won’t close deals or ship products. But it protects the business you’re building from preventable disasters.

We’ve seen too many capable, hardworking business owners get blindsided by compliance issues they didn’t know existed or didn’t prioritize correctly. The irony is that the time and money spent on a formal risk assessment is a fraction of what they pay in consequences later.

Start simple. Use a basic template. Focus on your top five risks. Document what you find. Review it quarterly. That’s better than what most of your competitors are doing.

And when that audit notice eventually arrives, or when a regulatory question comes up, or when your insurance company asks about your compliance program, you’ll have an answer that isn’t “we’re working on it.”

You’ll know your risks. You’ll know your gaps. And you’ll have a plan.

That’s the difference between guessing and managing.

Citations

- Gartner, “SMB Compliance Incident Report,” 2024.

- Ponemon Institute, “Cost of Compliance for Small and Medium Businesses,” 2024.

- U.S. Department of Labor, “Wage and Hour Division Enforcement Results,” 2024.